Introduction: Why Most People Struggle with Money

Financial literacy basics are essential for anyone who wants to manage money smartly and build a secure future.

Imagine this: a university student lands their first part-time job. For the first time in life, they have their own money. It feels exciting—freedom, independence, and endless possibilities.

But within a few weeks, the money is gone.

Food deliveries, subscriptions, hangouts, and random online shopping—each expense seems small. But together, they quietly drain the entire account balance.

Then comes the stress:

“Where did my money go?”

If this situation sounds familiar, you’re not alone.

This is precisely how most people begin their financial journey: confused, unprepared, and overwhelmed.

Here’s the truth:

- It’s not about how much money you earn

- It’s about how well you manage it

And this is where financial literacy basics come into play.

What are financial literacy basics?

Financial literacy is the ability to understand and effectively use financial skills, such as

- Budgeting

- Saving

- Investing

- Debt management

- Banking knowledge

In simple words:

Financial literacy means making your money work for you, not against you.

A financially literate person:

- Knows where their money is going

- Plans for the future

- Avoids unnecessary debt

- Makes informed financial decisions

Why Financial Literacy is Important in Everyday Life

Most people focus only on earning money. But without financial knowledge, even a high income can disappear quickly.

Common Problems Without Financial Literacy:

- Living paycheck to paycheck

- Falling into debt traps

- No savings for emergencies

- Financial stress and anxiety

- Poor long-term planning

Financial literacy helps you:

Key Benefits:

- Better control over your money

- Reduced financial stress

- Improved decision-making

- Faster financial growth

- Strong financial security

According to global studies, people with financial knowledge are more likely to save regularly and avoid high-interest debt.

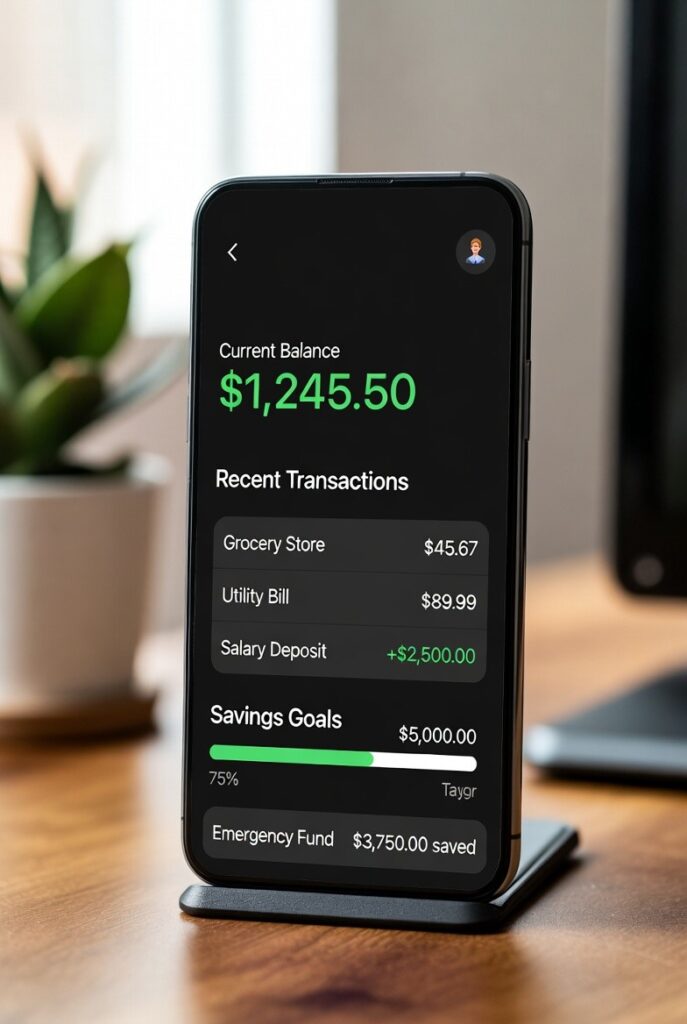

Understanding Money Management Basics

Money management is the foundation of financial literacy.

It includes:

- Tracking income

- Controlling expenses

- Planning financial goals

A simple rule:

Spend less than you earn and invest the difference.

Sounds simple—but most people fail because they don’t track their money.

If you don’t track your money, you lose control of it.

Financial Literacy Basics: Budgeting Guide

Budgeting is one of the most important financial skills you can learn.

A budget tells your money where to go instead of wondering where it went.

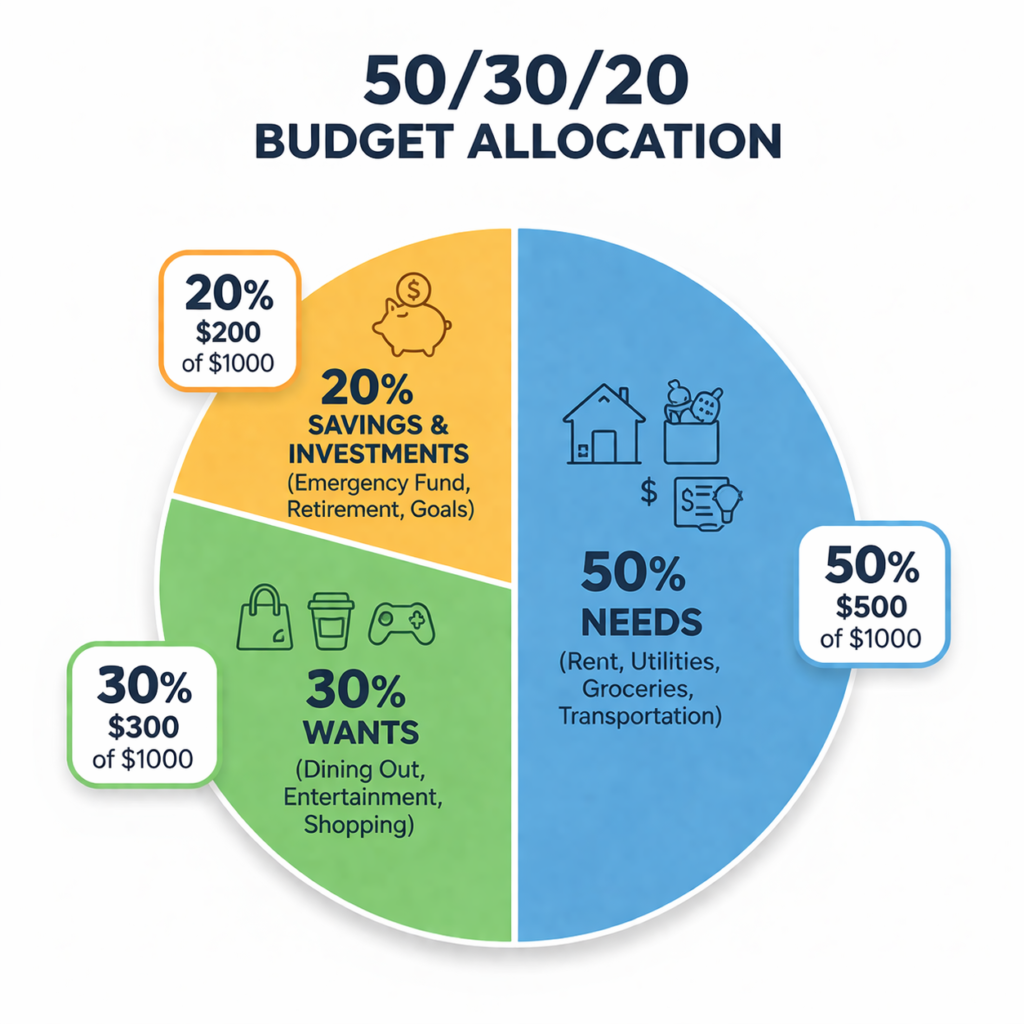

The 50/30/20 Rule

One of the most popular budgeting methods:

- 50% Needs (rent, food, bills)

- 30% Wants (entertainment, shopping)

- 20% Savings & Investments

Example Budget

If your monthly income is $1000:

- Needs → $500

- Wants → $300

- Savings → $200

Practical Budgeting Tips

- Track your daily expenses

- Use budgeting apps or Excel

- Avoid emotional spending

- Review your budget every month

- Set spending limits

Small changes in budgeting can completely transform your financial life.

Financial Literacy Basics: Saving Strategies

Saving money is not just about putting cash aside—it’s about securing your future.

How Much Should You Save?

Experts recommend saving:

At least 20% of your income

But if you’re starting:

Even 5–10% is enough

Types of Savings

Emergency Fund

Covers unexpected expenses

Target: 3–6 months of expenses

Short-Term Savings

Travel, gadgets, events

Long-Term Savings

House, retirement, business

Smart Saving Strategies

Automate your savings

Use separate bank accounts

Set clear financial goals

Avoid impulse buying

Save before spending

Rule: Pay yourself first.

Financial Literacy Basics: Investing for Beginners

Saving protects your money.

Investing grows your money.

Investing means putting money into assets like the following:

Stocks

Mutual funds

Real estate

Bonds

The Power of Compounding

Compounding means:

Your money earns returns… and those returns earn more returns.

Example:

If you invest monthly, your wealth grows faster over time—even with small amounts.

Basic Investing Rules

- Start early

- Think long-term

- Diversify investments

- Avoid emotional decisions

- Learn before investing

Important:

Investing without knowledge is risky.

Understanding Debt and Credit

Debt is borrowed money that must be repaid.

But not all debt is bad.

Good Debt vs Bad Debt

| Feature | Good Debt | Bad Debt |

|---|---|---|

| Purpose | Wealth creation | Consumption |

| Interest | Low | High |

| Outcome | Asset building | Financial stress |

Examples:

Good Debt:

- Student loans

- Home loans

- Business loans

Bad Debt:

- Credit card debt

- High-interest loans

- Buy-now-pay-later traps

Smart rule:

Use debt to build assets, not to fund a lifestyle.

Banking Fundamentals You Must Know

Banks play a key role in managing money.

Important Banking Concepts:

- Savings account

- Current account

- Interest rates

- Online banking

- Mobile banking

Why Banking Matters:

- Safe money storage

- Easy transactions

- Access to loans

- Financial tracking

Understanding banking makes money management easier and more efficient.

Common Financial Mistakes People Make

Even educated people make financial mistakes.

Most Common Mistakes:

- Not tracking expenses

- Overspending on wants

- Not saving money

- Using too much credit

- Investing without knowledge

Avoiding these mistakes can significantly improve your financial health.

Step-by-Step Guide to Improve Financial Literacy

Let’s make it practical.

Step 1: Track Your Spending

Write down every expense for 7 days.

Step 2: Create a Budget

Use the 50/30/20 rule.

Step 3: Start Saving

Even small amounts matter.

Step 4: Learn Investing Basics

Start with simple options.

Step 5: Avoid Debt Traps

Use credit wisely.

Step 6: Keep Learning

Read blogs, watch videos, and improve knowledge.

Weekly Financial Improvement Plan

Make it a habit:

Monday: Track expenses

Tuesday: Review budget

Wednesday: Cut unnecessary spending

Thursday: Learn investing

Friday: Save money

Saturday: Review progress

Sunday: Plan next week

Financial Literacy Comparison: Saving vs Investing

| Concept | Saving | Investing |

|---|---|---|

| Risk | Very Low | Medium–High |

| Return | Low | High Potential |

| Purpose | Safety | Growth |

Financial Literacy for Students

Students often struggle the most with money.

Why?

- Limited income

- High expenses

- No financial knowledge

Tips for Students:

- Create a simple budget

- Avoid unnecessary spending

- Use student discounts

- Start saving early

- Learn investing basics

Starting early gives a huge advantage in life.

Financial Habits That Build Wealth

Success comes from habits, not luck.

Powerful Financial Habits:

- Track every expense

- Save regularly

- Invest consistently

- Avoid unnecessary debt

- Think long-term

Small habits = Big financial results

FAQs (People Also Ask)

1. What is financial literacy in simple words?

It is the ability to understand and manage money effectively.

2. Why is financial literacy important?

It helps you avoid debt, save money, and grow wealth.

3. How can beginners learn financial literacy?

Start with budgeting, saving, and basic investing.

4. What are basic money skills?

Budgeting, saving, investing, and debt control.

5. Can students learn financial literacy?

Yes, and they should start as early as possible.

Conclusion: Take Control of Your Financial Future

Now that you understand financial literacy basics, one simple truth stands out: your financial future depends on the everyday choices you make, not on luck, not on timing, and not even on how much you earn.

Many people spend years waiting for the “right time” to start managing their money. They think, “I’ll start saving when I earn more” or “I’ll invest when I have extra cash.” But that perfect moment rarely comes. The reality is financial control doesn’t start with a high income; it starts with small, intentional actions.

You don’t need to change your entire life in one day. Just begin with awareness. Pay attention to where your money is going. Notice your spending habits. Start questioning small expenses that don’t really add value to your life. Then slowly introduce better habits like saving a little before spending, avoiding unnecessary purchases, and planning your finances instead of reacting to them.

It’s also important to accept that mistakes are part of the process. Maybe you’ll overspend one month or skip your savings goal; that’s normal. What matters is that you don’t give up. Every mistake teaches you something, and every step forward, no matter how small, brings you closer to financial stability.

Over time, these small efforts start to compound. You become more confident, more aware, and more in control. Money stops feeling like a constant stress and starts becoming a tool you can use to build the life you want.

Start small. Stay consistent. Think long-term.

Because at the end of the day, every financially strong person you see today started exactly where you are, without all the answers, but with the decision to learn and improve.

Now it’s your turn. Take that first step, stay committed, and slowly create a future where your money works for you, not the other way around.

Internal Resources

Greed vs Discipline in Investing: 7 Proven Strategies to Control Emotions and Build Wealth

Best Bank for Beginners: Tips, Safety, and Rewards | WealthGuideHub